Widow’s MIL Pays for Funeral, Furious After Discovering Son’s Life Insurance Payout

A grieving widow in her 40s is going through a very difficult situation after the sudden death of her husband. After his passing, she became involved in a serious family conflict with her late husband’s mother over life insurance money and funeral expenses.

Right after the husband died, the mother-in-law offered to pay for the funeral costs. The widow was emotional and accepted the help at that time. She was not in a stable mindset and was focused on handling the loss and arranging the funeral.

Months later, the widow remembered that there was a life insurance policy in her husband’s name, and she became the main beneficiary. This money was meant to help her rebuild her life, manage financial stability, and possibly move closer to family for support after the loss.

When the mother-in-law found out about the life insurance payout, she became upset and demanded that the widow repay the funeral costs. She also accused her of being selfish for keeping the insurance money. The widow feels confused because she believes the payout is important for her future and recovery.

This situation has created emotional stress and a family dispute over life insurance claims, funeral expenses, and financial responsibility after death. It highlights how grief, money, and family expectations can lead to serious conflict during already painful times.

It was a severe blow for the woman, and she was incredibly thankful to her MIL for volunteering to cover all the funeral expenses

Dealing With Grief, Funeral Costs, and Life Insurance Money (Simple Guide)

When a family member dies, emotions are very high. At the same time, there can also be financial stress, funeral expenses, and family conflict.

This situation becomes even more complicated when life insurance money and funeral costs are involved.

💰 1. The Cost of Funerals

Funerals are very expensive in many countries.

In the United States, the average funeral cost is around $7,000 to $12,000, according to the National Funeral Directors Association.

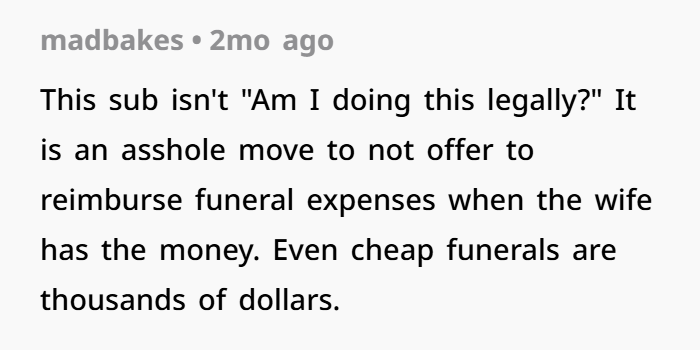

Because of this high cost, families often struggle with funeral planning and end-of-life expenses. Sometimes one family member may offer to pay, but it can still lead to misunderstandings if roles were not clearly discussed earlier.

⚖️ 2. Life Insurance and Legal Rights

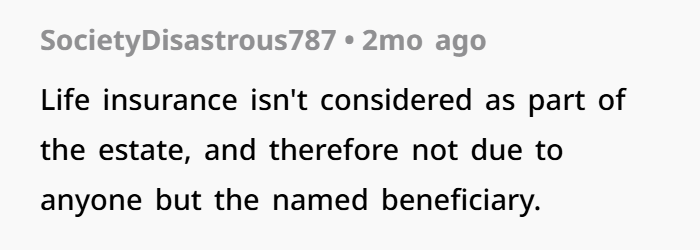

Life insurance money is usually paid directly to the named beneficiary in the policy.

This means:

- The beneficiary legally receives the money

- They can use it for living expenses, debts, or future needs

- They are not required to spend it on funeral costs

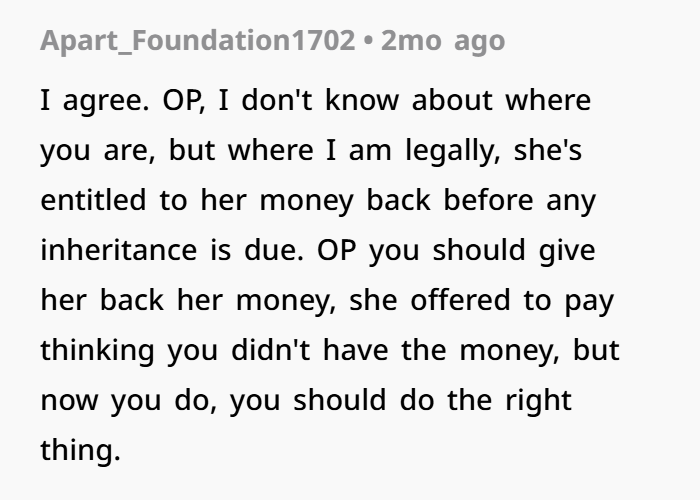

According to financial education sources like Investopedia, unless there was a written agreement, the beneficiary does not have to reimburse funeral expenses.

So legally, the widow is allowed to keep and use the insurance money.

🧠 3. Emotional and Ethical Issues

Even if something is legal, it can still feel emotionally difficult.

In this situation:

- The mother-in-law is grieving

- The widow is also grieving her husband

- There is stress about money and funeral costs

This can create tension and misunderstanding. In grief and family conflict situations, emotions like sadness, anger, and frustration can make communication harder.

The mother-in-law may feel hurt or overwhelmed, while the widow is trying to manage her own future and financial stability.

🏠 4. Why Life Insurance Exists

Life insurance is meant to help the surviving person after a death.

It is often used for:

- Rent or housing costs

- Daily living expenses

- Paying debts

- Financial stability after loss

This is part of financial planning after death and estate management.

So the money is not only about funeral costs—it is also meant to support long-term survival.

🤝 5. Possible Ways to Reduce Conflict

Even when someone is legally right, families may still try to find peace.

Some possible steps include:

✔ Open communication

Talking calmly about feelings and financial concerns can help reduce tension.

✔ Partial support (if possible)

The widow may choose to offer a small amount to help with funeral expenses, even if not required.

✔ Mediation or counseling

A neutral third person, such as a family counselor or mediator, can help both sides talk more clearly.

📚 6. Why These Conflicts Happen

Many estate planning and financial conflict studies show that problems often happen when:

- Money expectations are not discussed early

- Grief affects decision-making

- Family roles and responsibilities are unclear

Clear communication before or after a loss can help avoid long-term disputes.

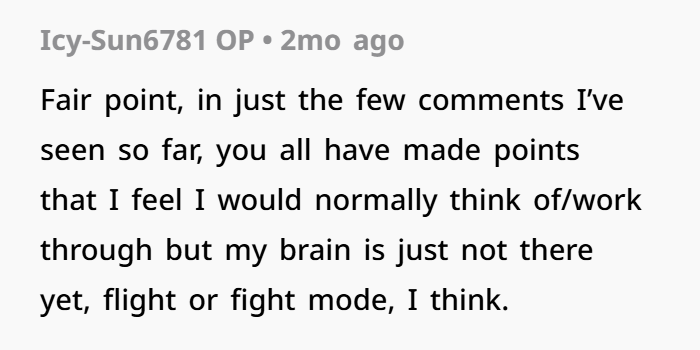

People in the comments were very divided, but most of them urged the author to pay the MIL back at least part of her expenses

🌿 Final Thoughts

This situation is both emotional and financial. The widow is legally allowed to keep the life insurance payout, but the mother-in-law is also dealing with grief and financial pressure.

In family financial planning and grief support situations, emotions often create misunderstandings even when no one is wrong legally.

While there is no legal requirement to share the money, small acts of empathy or communication may help reduce conflict and support healing for both sides.