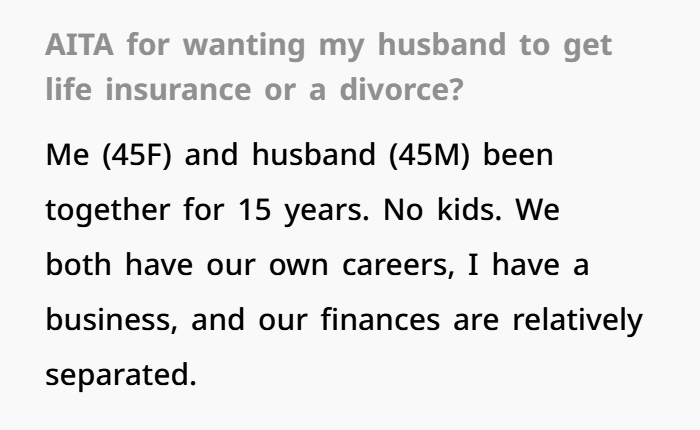

AITA for Telling My Husband It’s Life Insurance or Divorce After His Family’s Cancer Diagnosis?

A 45-year-old business owner believed she was being responsible when she talked to her husband about getting life insurance and disability insurance. Her concerns grew after her brother-in-law was diagnosed with pancreatic cancer, and doctors suggested genetic testing because of a strong family history. The news made her think about possible future health problems and the importance of financial planning. Having watched her mother struggle financially while caring for a seriously ill spouse, she understood how quickly medical bills, healthcare costs, and lost income can create financial stress. For her, discussing insurance coverage was not about money or greed. It was about protecting their financial security, avoiding medical debt, and preparing for unexpected challenges.

Her husband saw the situation very differently. He brushed aside her concerns and joked that she could support him financially if he ever became unable to work. He also joked that if he became disabled, he would simply spend his days playing video games. His comments made her feel that he was not taking important issues like disability coverage, life insurance, and long-term financial planning seriously. Frustrated by what she viewed as a lack of preparation, she suggested an unusual solution: getting a legal divorce on paper while continuing their relationship exactly as it was. Her goal was not to end the marriage but to protect her business, personal assets, retirement savings, and financial future from potential healthcare expenses. Now she is wondering whether she pushed the issue too hard or whether her husband is avoiding a very real financial risk that could affect both of their lives.

This story is not really just about life insurance.

At least not completely.

On the surface, it looks like a disagreement about financial planning, disability insurance, estate planning, long-term care costs, and asset protection. These are all important topics, especially when a serious health condition enters the picture.

But underneath those discussions is something much more personal.

Fear.

And both spouses seem to be dealing with that fear in very different ways.

The wife sees a serious warning sign. Her husband’s brother has been diagnosed with pancreatic cancer. His father also had the disease, and another family member was affected as well. Because of this family history, doctors recommended genetic testing and closer health monitoring.

For someone who has already seen the impact of a major illness, these concerns are difficult to ignore.

Her reaction becomes easier to understand when viewed from that perspective.

She watched her mother become a full-time caregiver for a sick spouse. She saw savings disappear, stress increase, and financial security become uncertain. She experienced how a long-term illness can affect an entire family.

Those experiences often stay with people for a long time.

Many people who have seen caregiver burnout firsthand become more aware of financial risks. They understand that a serious illness can affect not only the patient but also a spouse, family finances, retirement plans, career goals, and emotional well-being.

Topics such as long-term care insurance, disability insurance, life insurance, estate planning, medical expenses, and asset protection may seem unimportant until someone faces those challenges personally.

Then those financial decisions suddenly become very important.

The wife is not only thinking about what could happen in the future.

She is thinking about everything that could happen before that.

She is thinking about medical appointments.

She is thinking about long-term care needs.

She is thinking about healthcare costs.

She is thinking about balancing her business responsibilities while caring for her husband.

Those are understandable concerns.

In fact, many financial advisors recommend that married couples discuss these situations before they happen. Planning ahead can make difficult situations easier to manage if they ever arise.

The husband’s reaction shows a very different way of handling the situation.

Instead of focusing on possible risks, he appears more relaxed and unconcerned.

Some people may see that as irresponsible.

Others may see it as avoidance.

There is an important difference between the two.

His comments about spending time playing video games if he became disabled may sound dismissive. However, people often use humor when talking about subjects that make them uncomfortable. Sometimes joking is a way of avoiding difficult emotions.

It is possible that he truly is not worried.

It is also possible that he feels worried but does not know how to express those feelings.

His family history may also play a role.

According to the story, his father was abusive, and his father’s death brought feelings of relief rather than sadness. Experiences like that can affect how someone responds to illness, family health concerns, and discussions about the future.

Not everyone reacts to health scares in the same way.

Family experiences can shape how people process difficult situations.

For some people, emotional distance becomes a coping strategy. They avoid focusing on painful topics because that feels safer than confronting them directly.

That does not necessarily mean his response is the healthiest one.

But it may help explain why he reacted the way he did.

The biggest challenge here may not be life insurance or disability coverage.

It may be communication.

The wife approached the conversation with urgency because she wants financial security and protection.

The husband responded by avoiding the topic because he may not want to focus on a future that has not happened.

As a result, neither person seems to fully understand what the other is trying to say.

When the wife talks about life insurance and financial planning, she may really be saying:

“I don’t want our family to face financial hardship.”

“I don’t want to lose everything we have worked for.”

“I want us to prepare for the future together.”

“I want peace of mind.”

At the same time, the husband may be thinking:

“I don’t want to spend my life worrying about something that may never happen.”

“I don’t want fear to control my decisions.”

“I want to focus on living my life today.”

Unfortunately, those deeper feelings are getting lost in the discussion.

Instead of talking about fears and concerns, they are arguing about insurance policies.

That is something many couples experience.

The practical issue often becomes a symbol for a much bigger emotional issue.

For the wife, life insurance, disability insurance, and estate planning represent responsibility, protection, and love.

For the husband, those same topics may feel connected to fear, illness, and uncertainty.

That difference may be why the conversation became so emotional.

Then the discussion moved to divorce.

To be clear, the wife was not talking about ending the relationship.

She was suggesting a legal divorce for financial protection while staying together as a couple.

That is an important distinction.

However, the word “divorce” can carry a lot of emotional weight.

Even if her idea was based on financial planning and asset protection, it is understandable why her husband reacted strongly.

For many people, hearing the words “insurance” and “divorce” in the same conversation can feel overwhelming.

How something is said can be just as important as what is being said.

Interestingly, the wife later discovered that there may be other options available. For example, some insurance policies can be purchased on a spouse with proper consent. That realization shifted her focus toward finding solutions instead of continuing the disagreement.

That may be the direction this couple needs to take next.

Not trying to win the argument.

Trying to understand each other.

The truth is that both people have valid points.

The wife is right that medical debt, long-term care costs, disability expenses, and lost income can create serious financial challenges. Ignoring those risks does not make them disappear.

The husband is also right that no one knows what the future holds. Constantly assuming the worst-case scenario can create unnecessary stress.

The real goal is finding a balance between preparation and peace of mind.

Most successful couples learn that preparing for risks does not mean expecting them to happen.

Buying life insurance does not mean you expect tragedy.

Creating an estate plan does not mean you expect bad news.

Discussing long-term care insurance does not mean illness is guaranteed.

It simply means you are planning responsibly while hoping for the best.

At its heart, this story feels less like a disagreement about money and more like two people dealing with uncertainty in different ways.

One person manages fear through planning.

The other manages fear by avoiding the topic.

Neither approach is perfect.

But if they can move past the insurance debate and talk openly about their concerns, they may discover they both want the same thing: a secure future, financial stability, and peace of mind together.

And sometimes, that understanding is the most valuable protection any marriage can have.

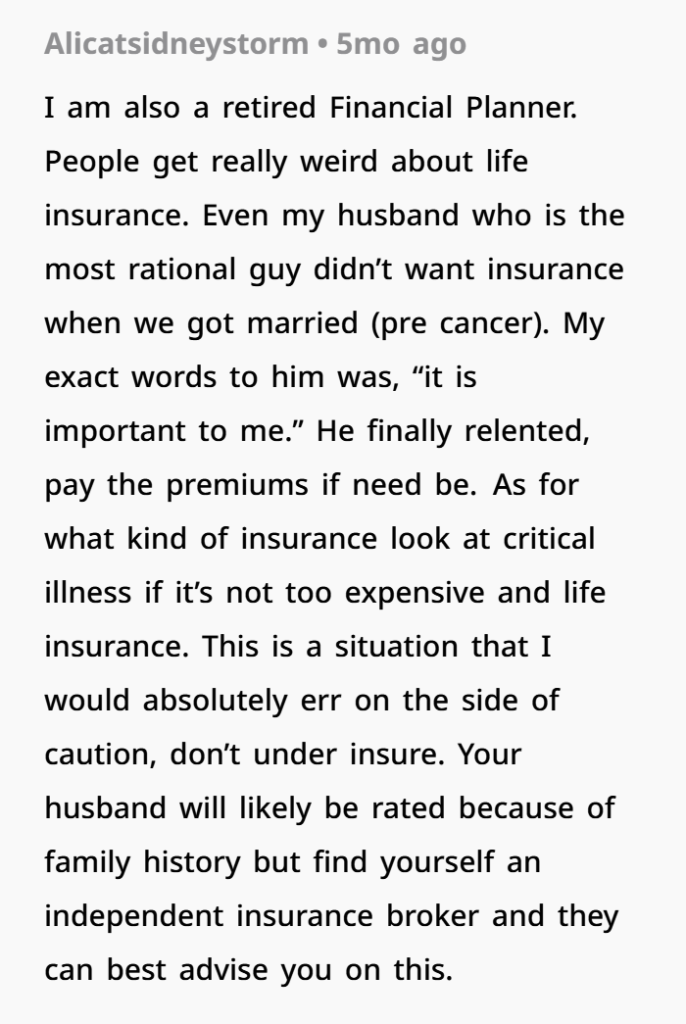

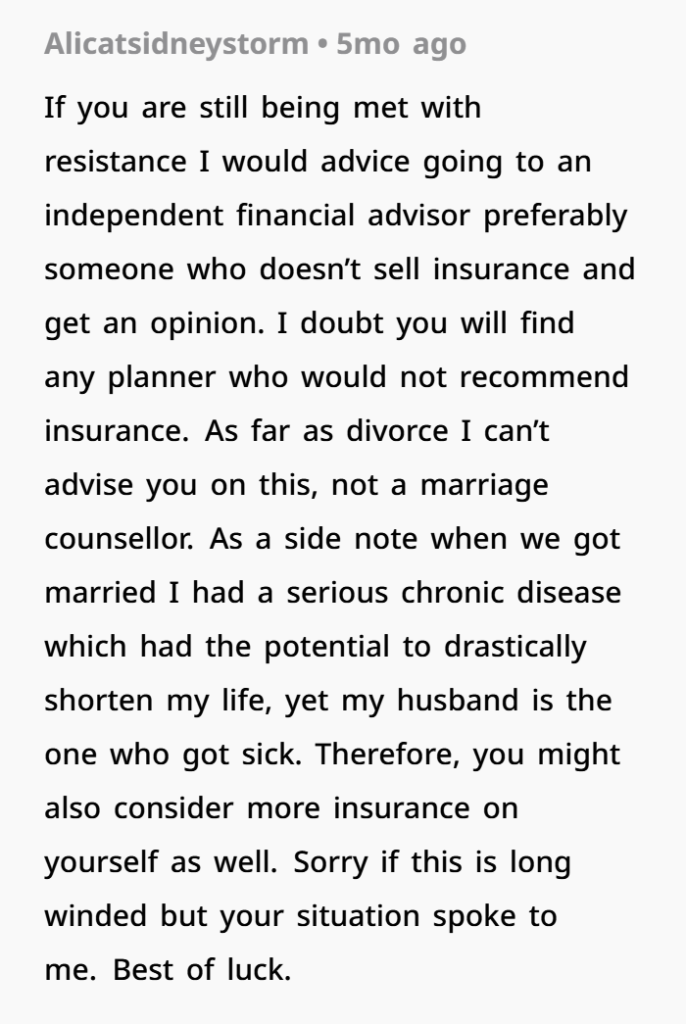

Top Comments From Readers