When My Husband Won’t Make Me a Beneficiary, I Made a Tough Choice

Blended families and financial planning can be messy, even in the best of relationships. One woman shared her story of being married for a little over a year, with two adult daughters from a previous marriage, when she discovered her husband refused to name her as the beneficiary on his life insurance policy. Having been through the loss of both her parents in her 30s, she was determined to protect her children and her husband from the kind of administrative and financial chaos she endured. So she set up policies to ensure everyone she cared about would be covered in the event of her death.

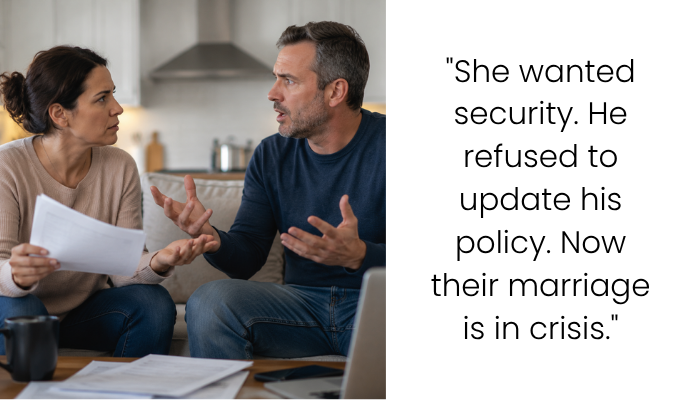

However, when she asked her husband to return the favor, he refused. His mother, who hasn’t been close to him in years, remains his sole beneficiary. Feeling unprotected if something happened to him, she canceled her life insurance for him and reallocated her other accounts to her children. Now, their marriage is tense, and he’s angry at her for “leaving him with nothing.” The situation raises questions about fairness, marital trust, and protecting your own financial security in blended families.

On the surface, this story might seem like a classic “wife vs. husband” conflict, but the real issues are about financial security, fairness, and risk management in marriage. Life insurance is not just a “nice to have”—it’s a safety net, and in blended families, it becomes even more critical.

The wife in this story had a clear rationale: she had lost both of her parents while still in her 30s, and as the legal next of kin, she had to handle their estates and pay expenses. That kind of experience leaves a lasting impression. She didn’t want her adult daughters to go through the same chaos, which is why she maintained and increased her life insurance for them. That’s responsible planning, not overreacting.

When she remarried, she took out a separate $100k policy for her husband, recognizing that if anything happened to her, he would be tasked with managing her affairs. The key here is proportionality: her husband earns less than she does, and the policy amount would help him cover expenses without going into debt. This isn’t about wealth or greed—it’s about making sure her spouse isn’t left in financial limbo.

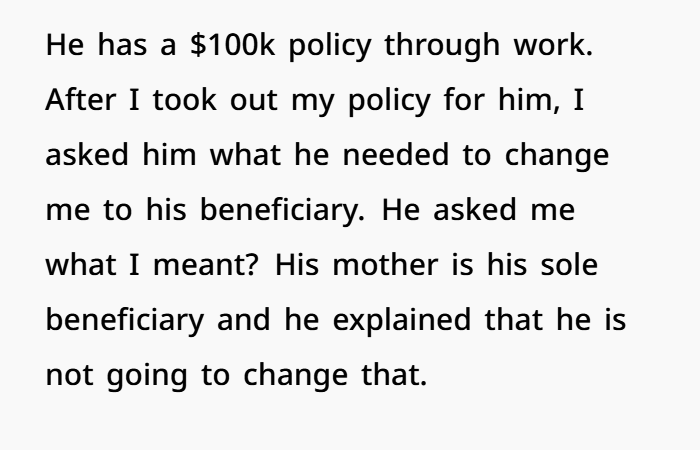

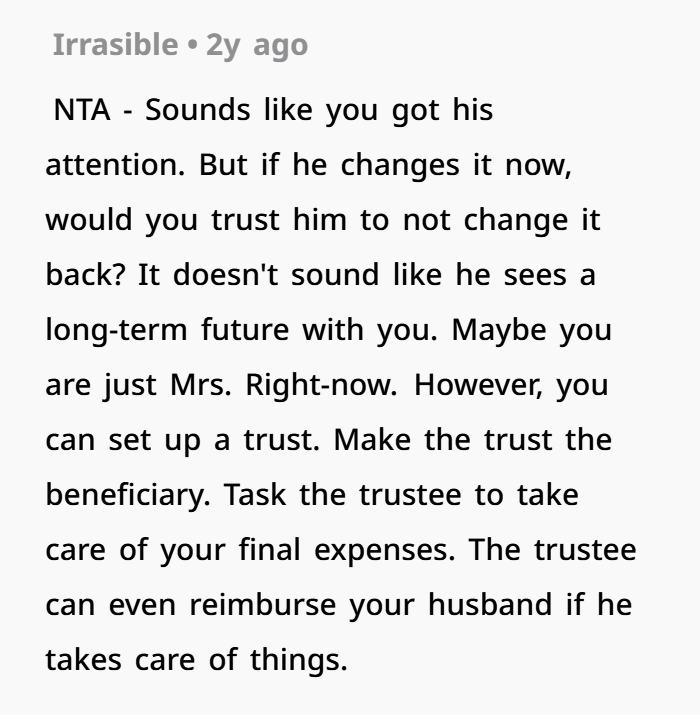

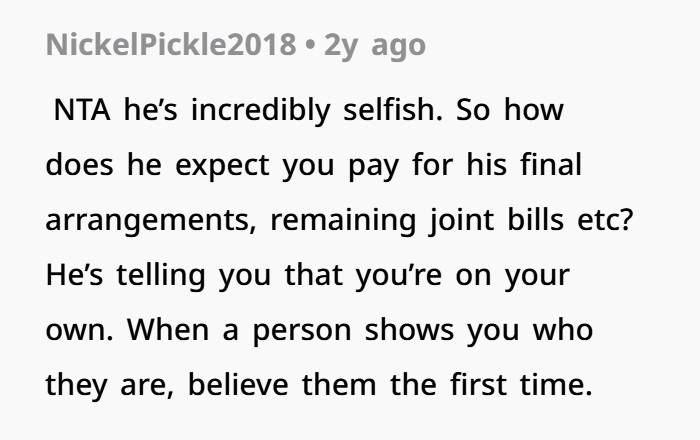

The problem started when she asked her husband to name her as a beneficiary on his work policy. His refusal—keeping his mother, who is financially well-off and distant, as the sole beneficiary—put her in a precarious position. From a financial planning perspective, this is a huge red flag. Estate lawyers and financial advisors often warn that a spouse who isn’t a beneficiary of their partner’s life insurance may have little recourse if something happens. Essentially, if he dies without changing his policy, she’s left navigating his estate alone, with zero guaranteed financial resources.

Many Reddit commenters would argue that a spouse refusing to name the other as a beneficiary is not just a financial misstep—it’s also a breach of marital trust. Marriage is supposed to involve shared responsibility, especially for financial safety nets like insurance. If one partner refuses to provide basic security for the other, it naturally causes tension.

Critics might say that canceling her policy was extreme or “petty,” but from her perspective, it’s logical. Why continue paying premiums for someone who refuses to protect you in return? Financial planning is not just about generosity—it’s about self-preservation. According to Certified Financial Planner professionals, it’s always recommended that couples coordinate their life insurance policies so that both partners are adequately protected.

There’s also the blended family factor. She has adult children from a previous marriage. While her husband and daughters have a friendly relationship, legally they aren’t next of kin. Her actions—redirecting her policies and POD accounts to her daughters—ensure her children are secure. This is a practical move that prioritizes responsibility over feelings.

Some might argue that she should have waited or negotiated more. Maybe she could have compromised with a smaller portion going to her, or an agreement outside of life insurance. But she tried for a year. Asking repeatedly is not unreasonable. His inaction shows a lack of urgency and consideration for her financial well-being. In contrast, she made sure her children and husband (with her policy) are covered; she didn’t act impulsively without reason.

Another angle is fairness and equity in a relationship. Marriage is a partnership. Financial planners often warn about “financial asymmetry”—when one partner is fully protected and the other is not. In this story, the asymmetry was glaring: she has policies for her children, for her husband, and for herself, while he has no obligation to do the same. That creates imbalance and resentment. Her decision to cancel coverage for him levels the playing field—it sends a clear message that protection should be mutual.

It’s also worth noting that life insurance isn’t just for immediate death benefits—it’s tied to estate planning, tax implications, and even emotional peace of mind. She has likely reduced her stress and uncertainty by redirecting her policies. The husband, on the other hand, is left facing the reality that if something happens, she may not have any obligation to sort out his affairs. That’s a consequence he created, not one she forced.

There’s a human element here, too. She’s not heartless; she tried to communicate, she considered his needs, and she clearly wants to protect him. But she also recognizes her own needs. In healthy marriages, both partners’ financial security should be respected. Refusing to be a beneficiary is a significant disregard for a spouse’s well-being.

Finally, it’s important to acknowledge the emotional toll. He’s angry, she’s frustrated, and the situation has created tension. However, her actions are consistent with risk management, legal safeguards, and self-respect. Many people online would say that being upset at someone for protecting themselves is unfair, especially when the “harm” she caused him is only that he now has to face the consequences of his own choices.

The Comments Are In

NTA (Not The Asshole).

She gave him plenty of notice, asked repeatedly, and explained her concerns. His refusal to name her as a beneficiary put her at financial risk. Canceling her policy for him and redirecting other assets to her children is a rational, responsible decision. Protecting herself and her children does not make her petty—it makes her prudent. He may feel “left with nothing,” but that’s a direct result of his own unwillingness to secure his spouse financially.

In blended families and second marriages, financial transparency and mutual protection are non-negotiable. Setting boundaries and ensuring your security is not selfish—it’s essential.