When My Husband Won’t Make Me a Beneficiary, I Made a Tough Choice

Blended families and financial planning can sometimes be complicated, even when a marriage is strong. One woman shared that she had been married for just over a year and has two adult daughters from a previous marriage. She was surprised to learn that her husband did not want to list her as the beneficiary on his life insurance policy. After losing both of her parents in her 30s, she understood how difficult financial planning, estate planning, and handling family finances can be after a loss. Because of that experience, she arranged her life insurance and financial accounts to help protect both her children and her husband.

When she asked her husband to do the same, he said no. Instead, he chose to keep his mother as the only beneficiary on his life insurance policy, even though they have not been very close for many years. Feeling uncertain about her own financial security, she decided to remove him from her life insurance coverage and updated other financial accounts so her children would receive those benefits. She felt it was important to protect her family and make sure her financial future was planned carefully.

As a result, their marriage has become strained. Her husband is upset and believes she has left him without financial support if something happens to her. The situation has started conversations about financial planning for married couples, life insurance beneficiaries, family protection, and the importance of trust in blended families. It also highlights how important it is for couples to have open discussions about money, estate planning, and long-term financial security.

At first glance, this may look like a simple disagreement between a husband and wife. However, the bigger issues are financial security, fair treatment, and smart financial planning. Life insurance is more than just an extra benefit. It is an important safety net, especially for blended families where financial responsibilities can be more complicated.

The wife had a good reason for her concerns. She lost both of her parents while she was still in her 30s. As their closest family member, she had to handle their estate planning, finances, and final expenses. That experience taught her how important it is to be prepared. Because of this, she kept strong life insurance coverage for her adult daughters to help protect them in the future. Her decision was based on responsible financial planning, not fear.

After getting remarried, she also purchased a separate $100,000 life insurance policy for her husband. She understood that if something happened to her, he would likely need to manage her affairs and cover unexpected costs. Since he earns less than she does, the policy could help provide financial security and prevent financial stress. Her goal was not to leave behind wealth but to make sure her spouse had support when needed.

The situation changed when she asked her husband to add her as a beneficiary on his work life insurance policy. He refused and decided to keep his mother as the only beneficiary. According to the story, his mother is financially comfortable and they are not very close. This left the wife feeling unprotected. Many financial advisors say that if a spouse is not listed as a beneficiary, they may face financial difficulties and legal challenges if their partner passes away. Without access to insurance benefits, she could be left handling everything on her own.

Many people believe that naming a spouse as a beneficiary is an important part of building trust in a marriage. Marriage often involves sharing responsibilities and creating financial safety nets together. When one partner chooses not to provide that protection, it can create concerns about both financial security and trust.

Some people may feel that canceling her policy for her husband was too harsh. However, from her point of view, it was a practical financial decision. She questioned why she should continue paying insurance premiums for someone who was unwilling to provide the same protection for her. Good personal finance decisions often involve balancing generosity with protecting your own future. Financial professionals frequently recommend that married couples review their insurance policies together to make sure both partners are covered.

The blended family situation also plays a role. The wife has adult daughters from a previous marriage. Although her husband gets along with them, they are not legally responsible for each other. By updating her beneficiaries and payable-on-death accounts, she ensured her children would receive financial support. This is a common estate planning strategy used to protect family members and avoid future complications.

Some people may think she should have continued negotiating. Perhaps they could have agreed to split benefits or create another financial arrangement. However, she had already discussed the issue for over a year. Wanting a clear answer was not unreasonable. While she made plans to protect both her children and husband, she felt that her husband did not show the same concern for her financial well-being.

Another important issue is fairness within a marriage. Financial planners often talk about financial balance between partners. In this case, the wife had plans in place to protect her children, herself, and her husband. Meanwhile, she felt she was receiving little protection in return. This imbalance naturally led to frustration. By changing her insurance coverage, she made it clear that financial protection should be a shared responsibility.

Life insurance also affects much more than a death benefit. It can be an important part of estate planning, retirement planning, tax planning, and long-term financial security. By updating her accounts, the wife may have gained greater peace of mind. At the same time, her husband now understands the possible consequences of not making similar arrangements for her.

There is also an emotional side to this situation. The wife clearly tried to communicate her concerns and wanted to protect her husband financially. At the same time, she recognized the importance of protecting herself. In a healthy relationship, both partners’ financial needs should be respected. Refusing to include a spouse as a beneficiary can leave the other person feeling unsupported and vulnerable.

In the end, the disagreement has caused stress for both of them. He is upset, and she is disappointed. Still, her actions reflect common financial planning principles such as risk management, financial protection, and personal responsibility. Many people would argue that taking steps to secure your own future is reasonable, especially when those decisions are based on careful planning rather than emotion. The situation highlights the importance of open conversations about life insurance, estate planning, and long-term financial security in any marriage.

The Comments Are In

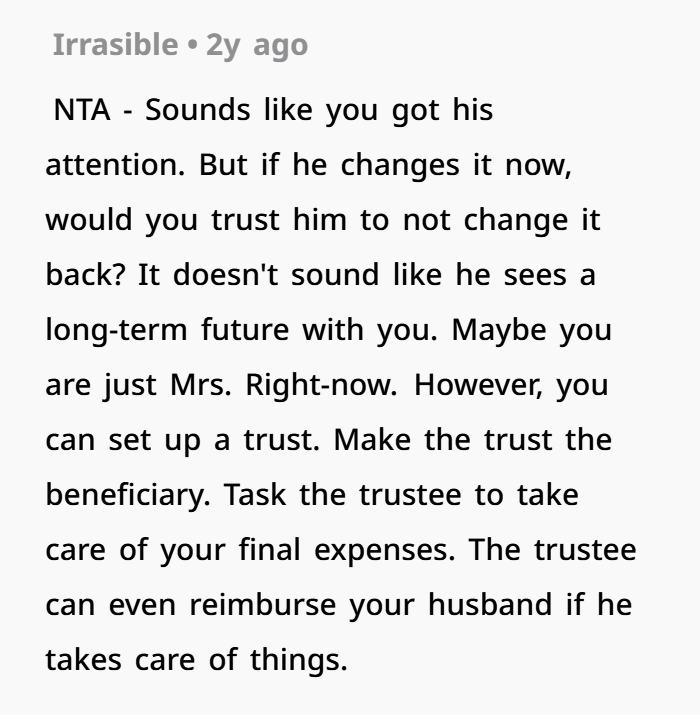

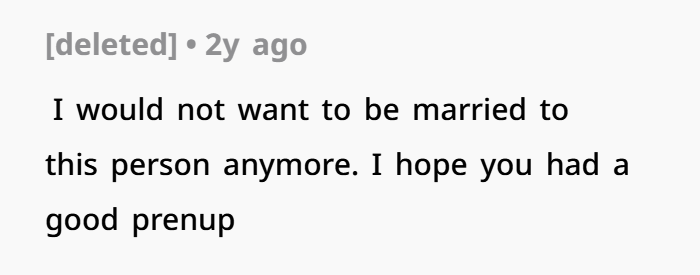

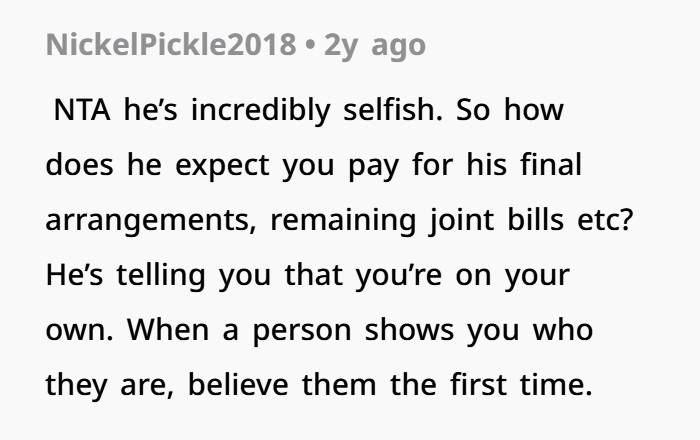

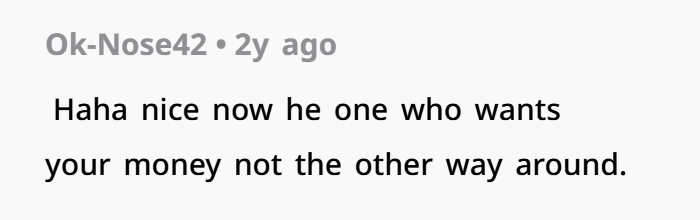

NTA (Not The Asshole).

She gave her husband plenty of time to make a decision. She talked to him several times and clearly explained why financial security was important to her. However, he chose not to add her as a beneficiary on his life insurance policy. Because of that, she felt it was necessary to review her own financial planning and make changes to protect herself and her children.

As a result, she decided to cancel the life insurance policy she had for him and update her other financial accounts so her children would receive those benefits. From a personal finance and estate planning perspective, this was a practical decision. Her goal was not to punish anyone but to make sure her family would have financial protection and long-term security if something unexpected happened.

Her husband may feel disappointed that he no longer has access to those benefits, but that situation developed because he chose not to provide the same level of financial protection for his spouse. Many financial advisors recommend that married couples discuss life insurance, beneficiaries, retirement planning, and estate planning together so both partners are protected.

This situation also highlights an important lesson for blended families and second marriages. Open communication, financial transparency, and mutual support are essential for building trust and financial stability. Setting healthy financial boundaries and protecting your future is not selfish. It is a responsible part of financial planning and helps create greater peace of mind for everyone involved.