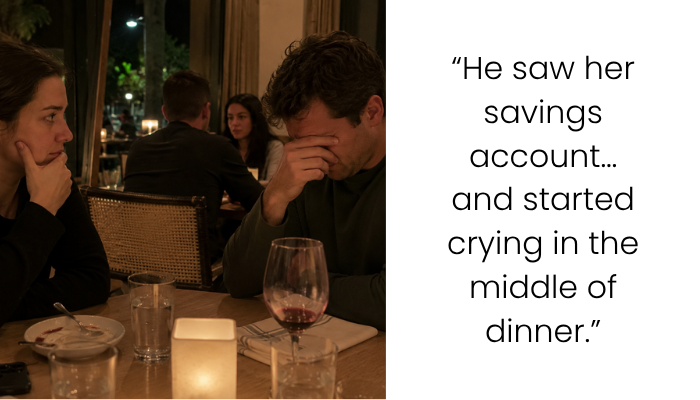

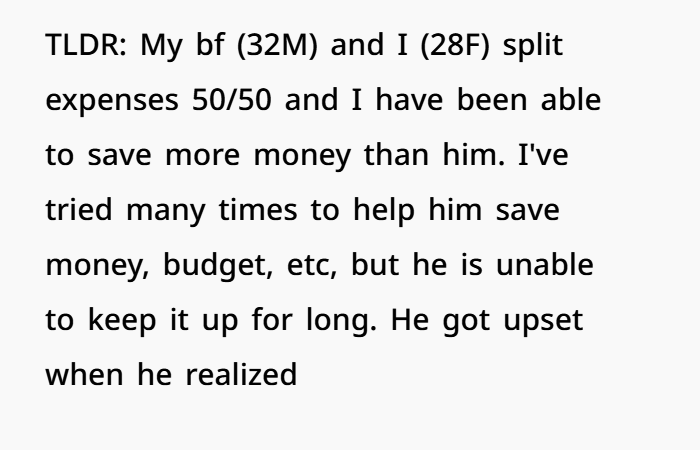

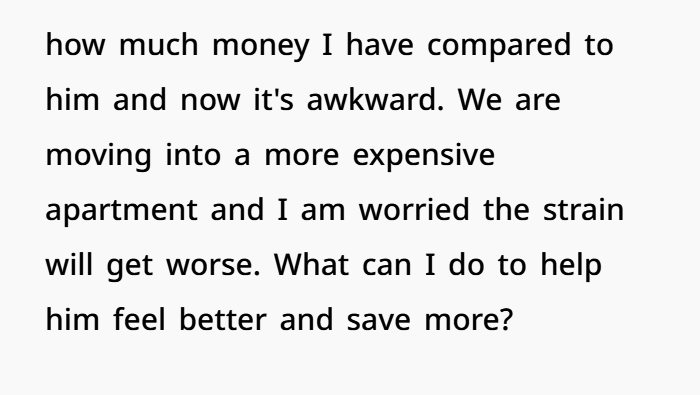

“My Boyfriend Cried When He Saw My Savings” — The Financial Reality Check That Changed Everything

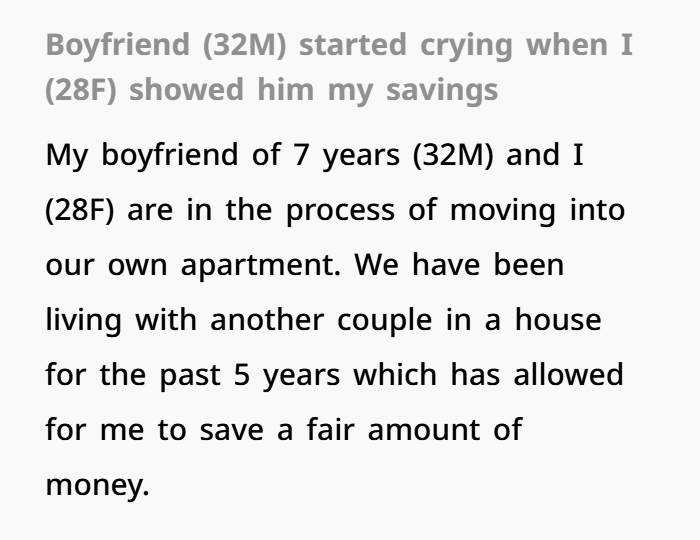

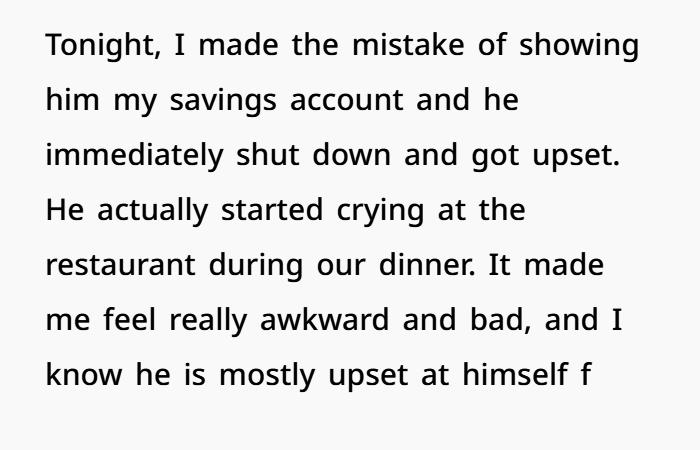

Money issues can sometimes stay hidden in a relationship for a long time before becoming a serious concern. In this story, a woman was discussing plans to move into a more expensive apartment with her boyfriend of seven years when she showed him her savings account. What seemed like a normal conversation about finances quickly became emotional. Instead of feeling excited about their future plans, her boyfriend became upset and overwhelmed by what he saw. The moment turned an ordinary financial discussion into a difficult conversation about money management, savings goals, and long-term financial planning.

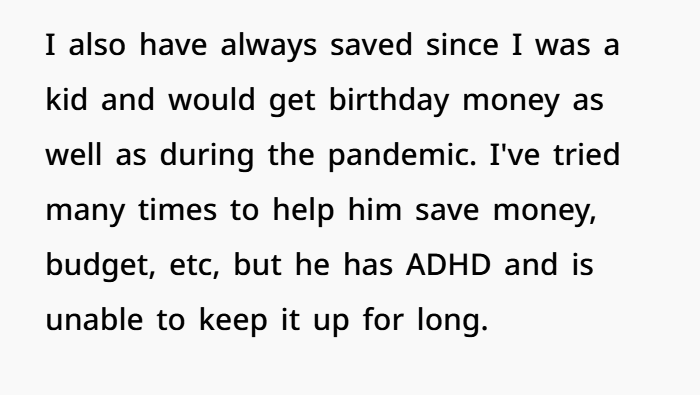

The situation was especially challenging because both partners earn similar incomes and have always shared living expenses equally. However, they have very different approaches to personal finance. The woman has focused on budgeting, saving money, and building financial security over time. Her boyfriend, on the other hand, has struggled with spending habits, financial organization, and consistency. Seeing the difference in their savings made him realize how differently they had managed their finances over the years. Now, the woman feels conflicted. She does not want her partner to feel discouraged, but she is also concerned about how financial compatibility, budgeting strategies, and future living expenses could affect their relationship moving forward. The story has sparked conversations about personal finance, wealth building, financial literacy, money management, savings accounts, financial planning, and the importance of open communication about finances in long-term relationships.

This story connected with many readers because it is about much more than money. At its core, it highlights important topics like financial planning, long-term goals, relationship trust, and personal responsibility. While the situation started with a simple conversation about savings, it quickly became clear that both partners were thinking about their future in very different ways.

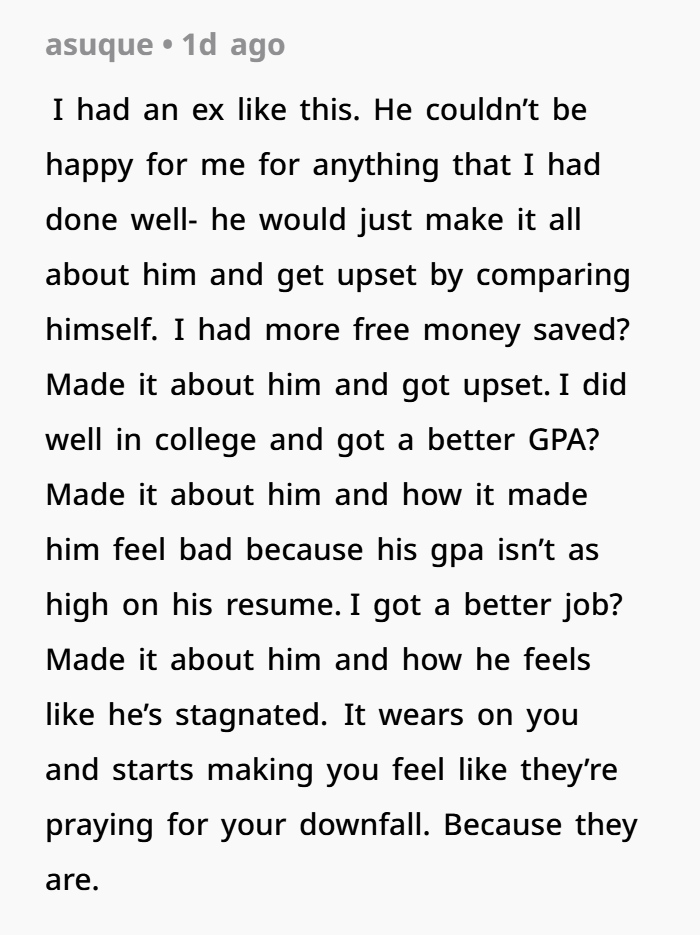

Many people felt that the boyfriend’s emotional reaction was not really about the amount of money in the savings account. Instead, it was about what those savings represented. For many adults, a strong savings account provides financial security, emergency protection, and peace of mind. Seeing a large difference in financial progress can sometimes be emotional, especially when both partners earn similar incomes.

One detail that stood out to readers was that the couple had shared expenses equally for years. Since neither partner appeared to have major financial advantages, many people believed the difference came from financial habits, budgeting choices, and long-term money management. Small financial decisions made consistently over time can have a major impact on personal wealth and financial stability.

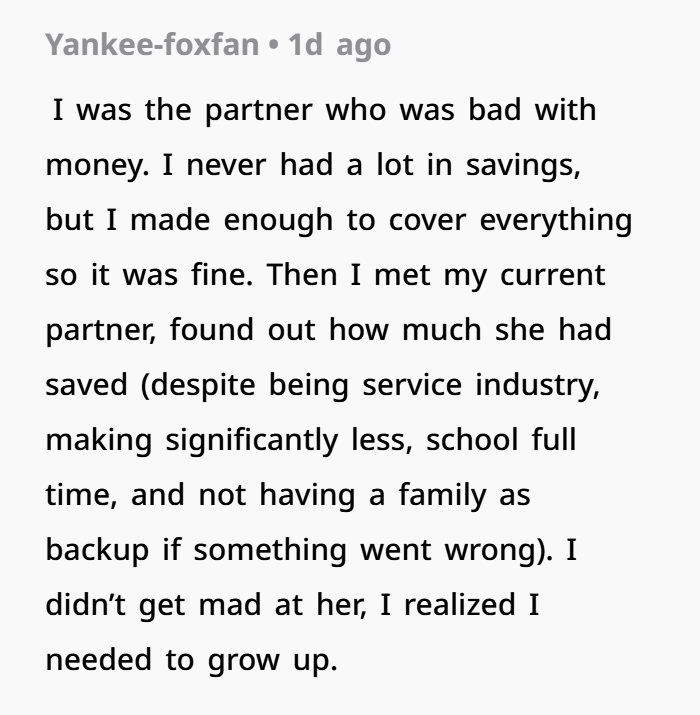

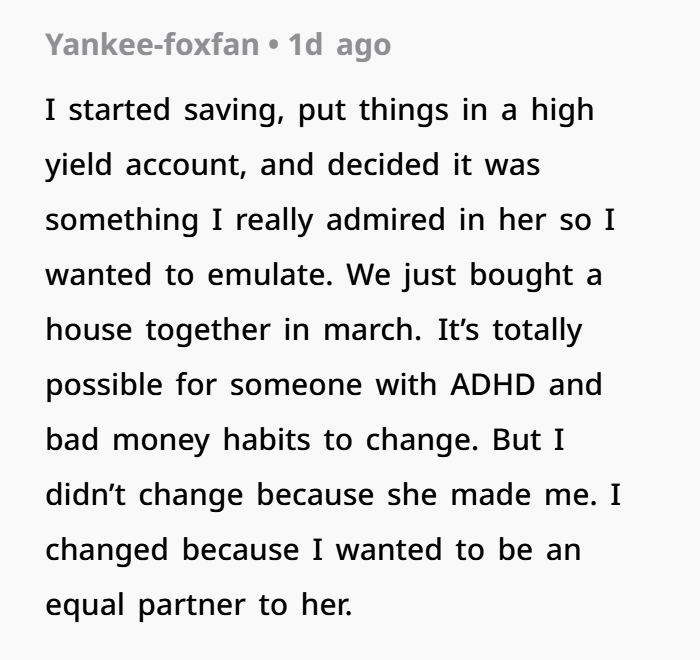

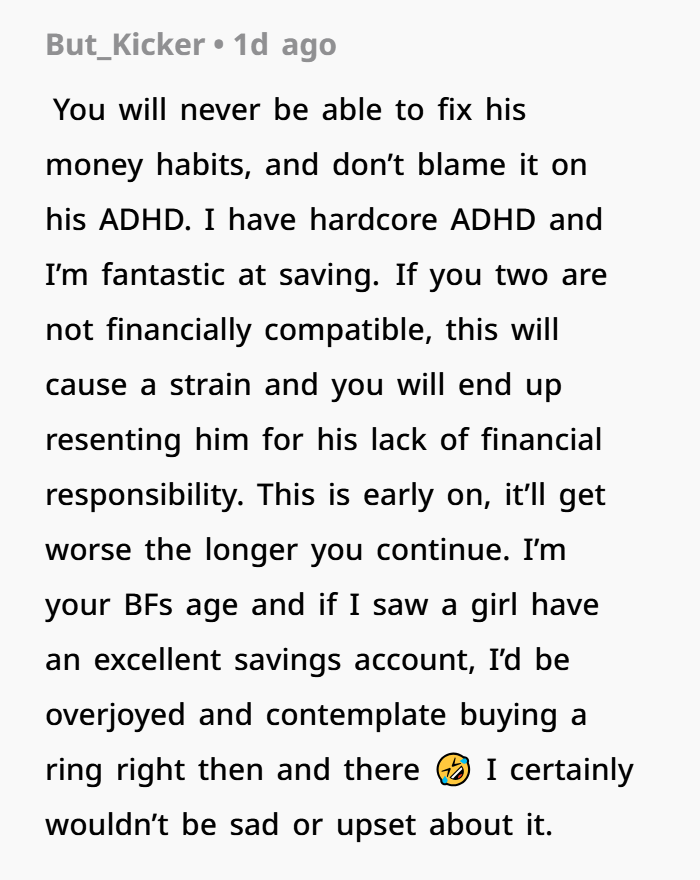

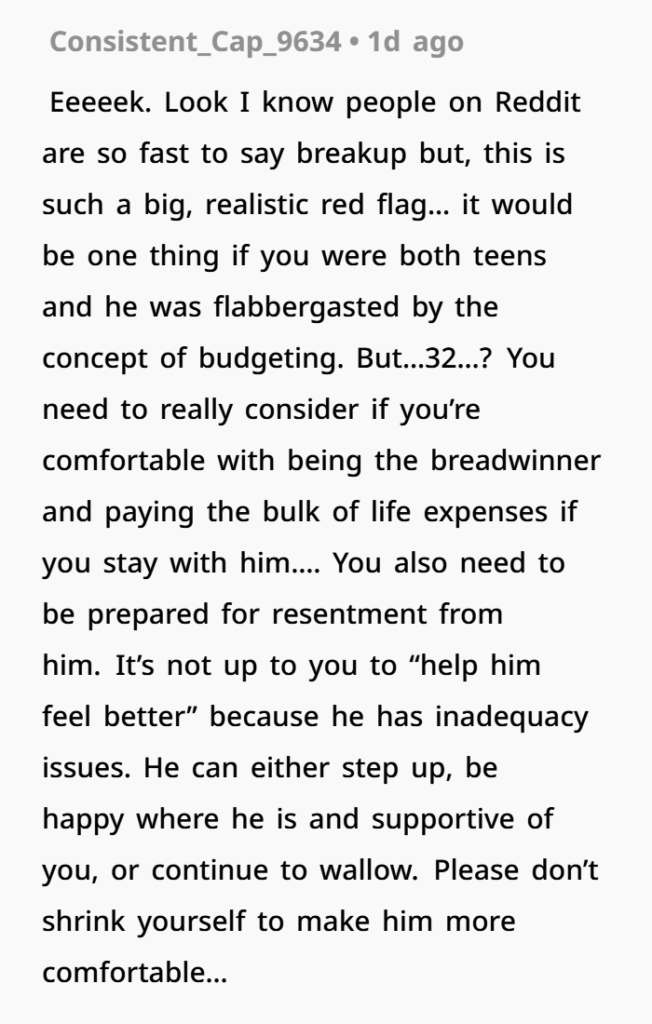

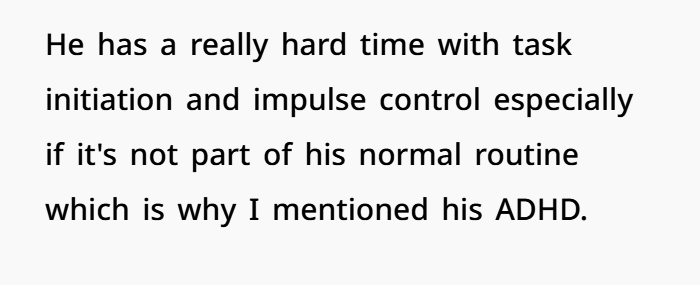

The discussion also included the challenges that some people face with organization, planning, and managing daily responsibilities. Many readers pointed out that attention-related challenges can sometimes affect budgeting, saving money, and staying on top of financial tasks. However, they also agreed that building healthy financial habits remains important for long-term success.

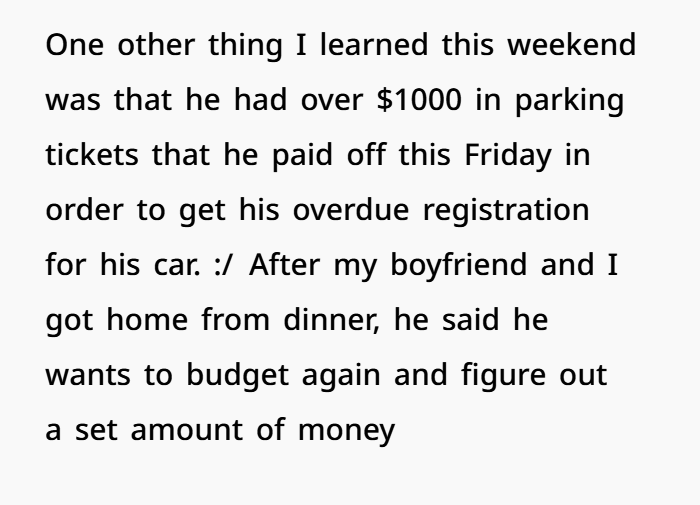

Another topic that received attention was the boyfriend’s reported difficulty handling financial responsibilities such as parking tickets, registrations, and other routine expenses. Readers noted that avoiding small financial tasks can sometimes lead to larger financial problems later. This is why financial literacy, budgeting tools, and money management systems are often recommended by personal finance experts.

Many commenters said the story highlighted the importance of financial compatibility in relationships. Couples do not need identical incomes to build a successful future together, but they often benefit from having similar views on budgeting, saving, investing, and financial planning. Shared financial goals can make it easier to manage housing costs, living expenses, and future responsibilities.

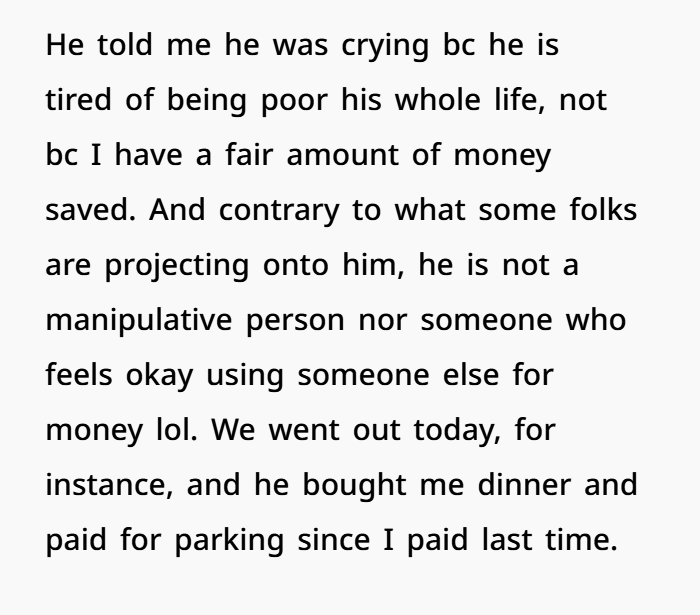

What stood out to many readers was that the woman did not seem angry or judgmental. Instead, she appeared concerned about the future and wanted to find a healthy solution. Some people felt this showed maturity, compassion, and a strong understanding of relationship dynamics.

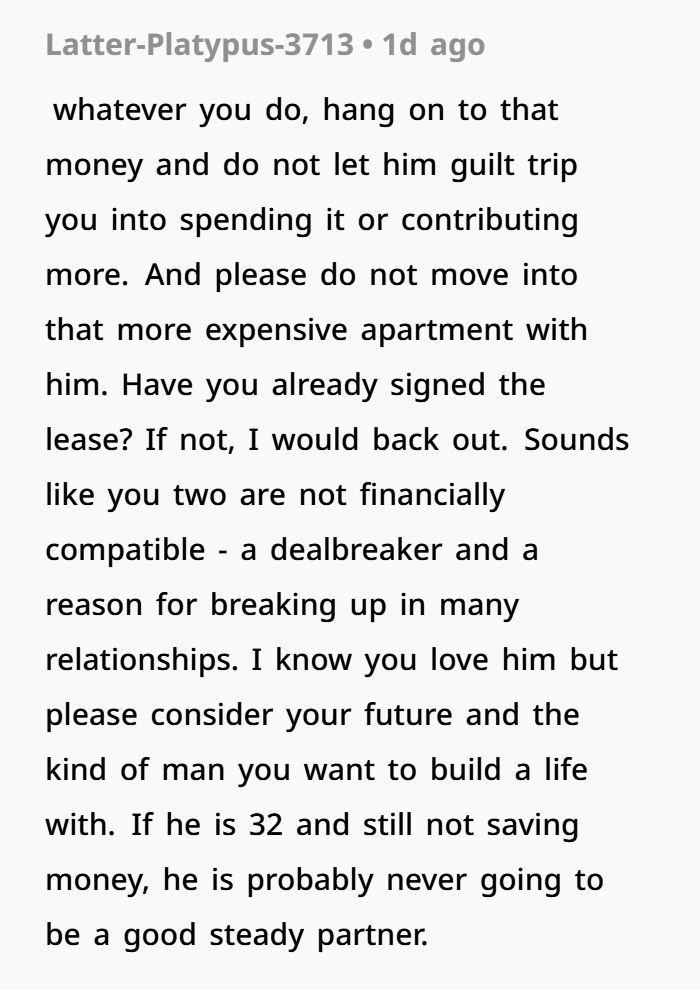

The upcoming move to a more expensive apartment also added pressure to the situation. Higher rent, larger utility bills, and increased living expenses often make financial differences more noticeable. As a result, conversations about budgeting, emergency funds, and financial security become more important.

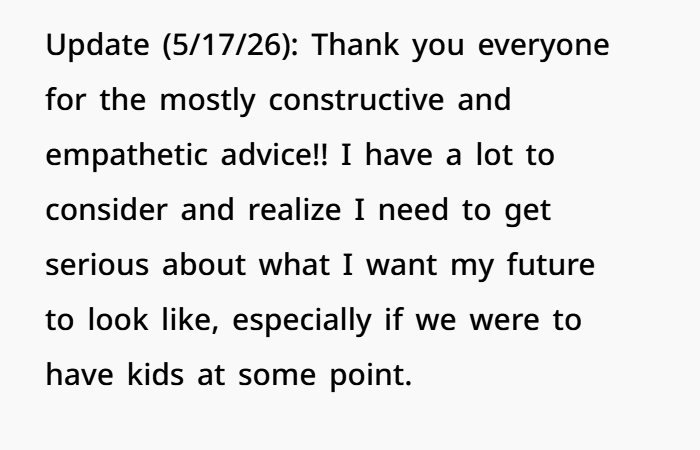

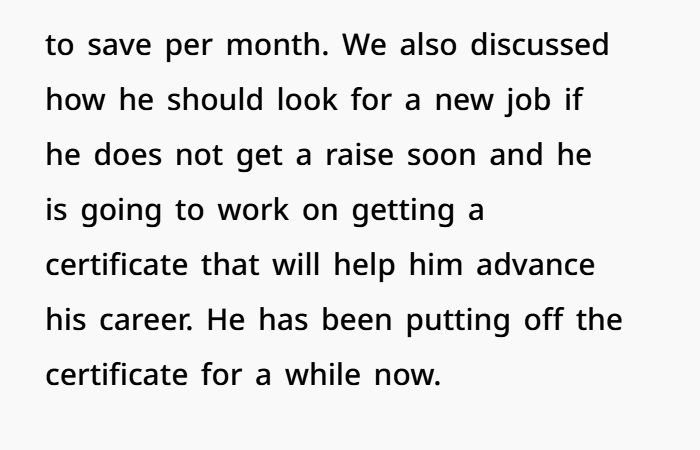

Readers also discussed the positive side of the story. According to the update, the boyfriend recognized that changes may be needed and expressed interest in improving his financial situation. He reportedly talked about career development, professional certifications, savings goals, and better budgeting strategies. Many people viewed this self-awareness as an encouraging first step.

At the same time, readers emphasized that long-term progress usually depends on consistent action rather than short-term motivation. Financial experts often recommend practical tools such as automatic savings transfers, budgeting apps, spending alerts, debt reduction plans, and financial coaching to help build stronger money habits over time.

Many people also felt that the woman should continue protecting her financial future while supporting her partner’s growth. Maintaining personal savings, avoiding unnecessary debt, and making thoughtful financial decisions can help create stability in any relationship.

Ultimately, the story sparked broader conversations about personal finance, wealth building, financial literacy, money management, relationship trust, and long-term financial security. Many readers agreed that successful relationships require more than love alone. Financial responsibility, communication, planning, and consistency are also important parts of building a stable future together.

Readers had plenty of thoughts to share, and the woman replied to some of their comments along the way