AITAH for Telling My Ex-Wife to Get Her Own Insurance After Our Divorce Filing?

Divorce is often more complicated than simply signing legal documents. Even after a couple separates, there can still be important financial matters, insurance coverage, shared responsibilities, and legal details that need to be resolved. These situations can sometimes create confusion about what is fair and what responsibilities remain after the relationship ends. That is exactly what happened to one Canadian man who had been living separately from his wife for more than a year and was finally moving forward with the divorce process.

The disagreement began when his ex-wife asked him to submit another therapy reimbursement claim through his health insurance plan. He agreed to process the current insurance claim but also reminded her that she would need to find her own health insurance coverage in the future. He explained that once the divorce was finalized, he planned to remove her from his employee benefits and insurance policy, which is a normal part of financial planning after divorce. However, his ex-wife did not react well to the conversation. She became upset and questioned whether he truly wanted to maintain the friendly relationship they had managed to preserve after their separation. Now he is wondering whether setting clear financial boundaries and discussing future insurance coverage was the right decision, or if it came across as insensitive during an already difficult divorce and family transition.

One of the most important things to understand in this story is that the disagreement was not really about a therapy reimbursement claim. The husband never refused to submit the current insurance claim. In fact, he agreed to process it. The real issue was about future expectations, financial planning, and setting healthy boundaries after a divorce.

When a marriage ends, people often have different ideas about what happens next. One person may expect support and shared benefits to continue for a while, while the other may believe it is time to separate finances and responsibilities. These different expectations can easily lead to misunderstandings and conflict.

In this situation, the husband’s message was fairly simple. He was not trying to punish his ex-wife or deny her access to the current claim. He was simply letting her know that she should start looking for her own health insurance coverage because he planned to remove her from his policy once the divorce became official.

From a financial planning perspective, this is a reasonable conversation to have.

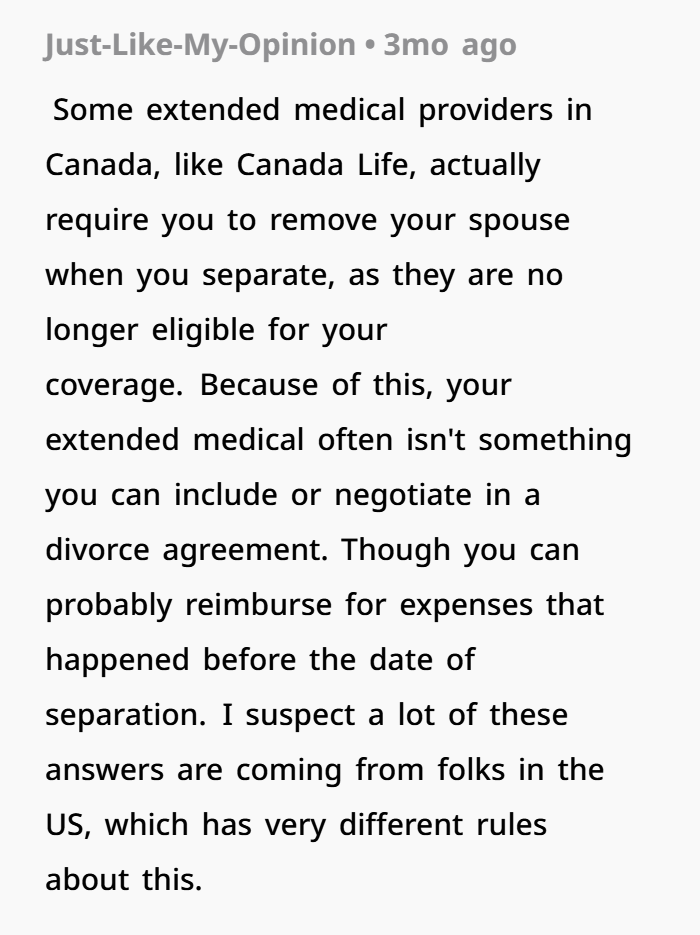

Health insurance, employee benefits, therapy coverage, dental insurance, and medical reimbursement plans are often tied to a legal marriage. Once a divorce is finalized, many insurance providers no longer allow an ex-spouse to remain on the policy. Because of this, divorce attorneys and financial advisors often recommend planning ahead and researching alternative healthcare coverage before the legal process is complete.

This becomes even more important when mental health services are involved.

Therapy, counseling, and other healthcare treatments can be expensive. Many people rely on insurance benefits to make these services affordable. Losing coverage without warning could create financial stress and interrupt important care. By discussing the upcoming change in advance, the husband was giving his ex-wife time to prepare and explore her options.

Imagine if he had never mentioned it.

If the divorce became final and the insurance coverage ended without notice, many people would likely argue that he should have warned her sooner. Instead, he chose to communicate openly about what would happen in the future.

His message was essentially: “I will process this claim, but please start planning for your own insurance coverage because this benefit will not last forever.”

That sounds more like responsible financial planning than cruelty.

Another important part of the story involves friendship after divorce.

His ex-wife questioned whether he truly wanted to remain friends. This is where emotions can become complicated. Many people struggle to separate friendship from financial support after a relationship ends.

Being friends with an ex-spouse can mean maintaining respect, kindness, and healthy communication. However, friendship does not automatically mean continuing every financial benefit that existed during the marriage.

Those are two very different things.

For example, most people would not expect an ex-spouse to continue paying household bills, sharing bank accounts, or providing unlimited financial support simply because they remain friendly. Health insurance coverage often falls into a similar category because it is connected to the legal marriage rather than the friendship itself.

The challenge is that healthcare feels personal.

When therapy, counseling, prescription medications, or medical treatments are involved, conversations about insurance benefits can feel emotional. What one person sees as a practical financial boundary may feel like rejection or loss to someone else.

That is why these discussions are often difficult.

Many divorce and family law professionals recommend setting clear expectations early. The longer someone depends on benefits provided by an ex-spouse, the harder the transition can become later. Establishing boundaries helps both people move forward and build financial independence.

There is also a practical legal side to consider.

Many insurance policies have strict eligibility requirements. Once a divorce is finalized, keeping an ex-spouse on a health insurance plan may no longer be allowed. Continuing coverage after eligibility ends can sometimes create administrative problems or insurance complications.

That is another reason why planning ahead is important.

The husband’s statement was not, “I am removing you today.”

Instead, it was closer to, “Please prepare because this will change in the future.”

Those are very different messages.

The timeline also matters. According to the story, the couple had already been living separately for more than a year before moving forward with the divorce. This was not a sudden breakup. Both individuals had time to begin adjusting to separate lives and planning for future financial responsibilities.

Because of that, discussing healthcare coverage, insurance benefits, and financial independence seems reasonable and practical.

Of course, there is another side to consider.

Even when people know a divorce is coming, certain milestones can still be emotional. Losing access to insurance benefits may feel like another reminder that the relationship is officially ending. That emotional reaction is understandable.

However, feeling upset does not automatically mean the conversation was wrong.

Some discussions are uncomfortable but necessary.

Healthy boundaries often require difficult conversations, especially during major life transitions such as divorce, financial separation, and estate planning.

Perhaps the strongest point in the husband’s favor is how he handled the situation. He agreed to process the current therapy claim, gave advance notice about future changes, and communicated openly instead of waiting until the last minute.

That approach shows consideration rather than hostility.

He did not deny assistance.

He did not create a surprise.

He simply explained what would happen once the divorce became final.

When viewed from that perspective, his actions seem less about cutting someone off and more about responsible divorce planning, healthcare coverage management, and financial independence.

At the end of the day, friendships can continue after divorce, but financial benefits tied to marriage often do not. Health insurance, therapy reimbursement, employee benefits, and medical coverage are usually connected to the legal relationship itself. When that relationship ends, it is normal for those arrangements to change as well.

Based on the facts presented, giving an ex-spouse advance notice about future insurance changes appears to be a practical and responsible step. It allows both people to prepare, make informed financial decisions, and move forward with greater stability and peace of mind.

What The Comments Reveal

Likely Reddit Verdict: NTA (Not The Ahole)**

The poster isn’t refusing the current reimbursement and isn’t removing coverage prematurely. He’s giving advance notice that his ex-wife needs to secure her own health insurance once the divorce is finalized. That’s a reasonable boundary, and honestly, it’s probably a conversation that needed to happen sooner rather than later.