AITAH for Refusing to Use My Entire Paycheck to Repay My Fiancé’s Family?

A young mother is wondering if she is wrong for refusing to give all of her paycheck toward debts that belong to her fiancé. The couple have been together since they were teenagers, but his grandparents have never fully supported their relationship. Over the years, they often criticized her, blamed her for family problems, and looked down on her for being a stay-at-home mom. However, the situation was much more complicated than it appeared.

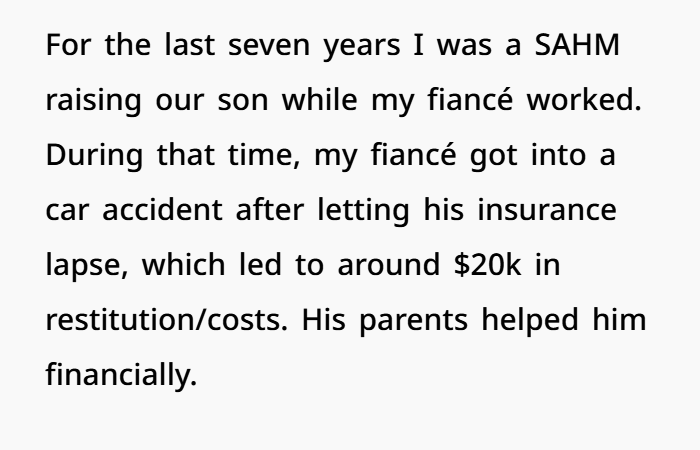

She became pregnant at 16 while working, but serious pregnancy complications forced her to leave her job. After their son was born, he developed health issues that required frequent medical appointments and extra care. Because childcare costs and daycare expenses were so high, the couple decided it made more financial sense for her to stay home while her fiancé worked and supported the household.

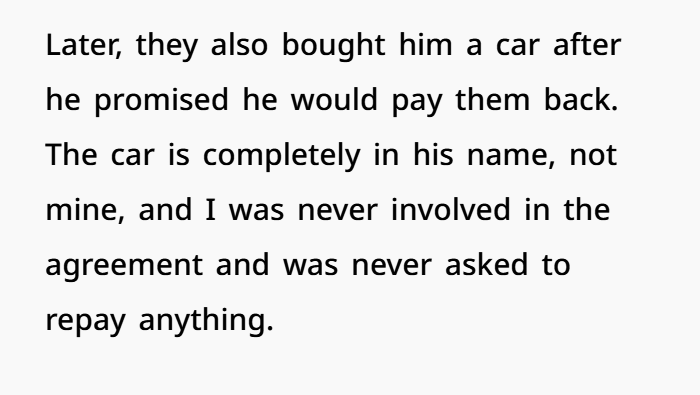

During that time, her fiancé made several financial mistakes. He allowed the family car insurance policy to lapse and later got into an accident. The incident resulted in significant expenses, legal costs, and restitution payments estimated between $15,000 and $20,000. His grandparents stepped in to help with the financial burden. They also purchased a vehicle for him with the understanding that he would repay the money over time.

Now that she has finally secured a new job and is earning an income again, his grandparents expect her paycheck to go directly toward paying off those debts. The problem is that she never agreed to borrow the money herself, nor was she involved in making those financial decisions. While she understands the importance of debt management and financial responsibility, she feels uncomfortable being expected to hand over every dollar she earns.

Instead, she wants to contribute to family finances, help cover household expenses, and work toward long-term financial planning for their future. She believes her income should support their child, daily living costs, savings goals, and overall financial stability rather than being completely redirected toward debts that were not originally hers.

The disagreement has now created tension within the family. His grandparents feel she should help repay the money because she benefits from the household finances. She feels that while she is willing to contribute fairly, expecting her entire paycheck is unreasonable. The situation has sparked a larger conversation about personal finance, shared financial responsibility, budgeting, family debt, and how couples should handle money when one partner’s obligations become a source of conflict.

This situation highlights a common issue in many families today: unpaid caregiving, financial pressure, and the hidden value of stay-at-home parenting. Many people hear the phrase “stay-at-home mom” and assume someone simply chose not to work. In reality, childcare costs can be extremely expensive. When a child has medical needs, staying home often becomes a practical family decision rather than a personal preference.

That is what makes this story more complicated. The fiancé’s grandparents seem to believe her staying home caused many of the family’s financial problems. But when you look at what happened, the biggest debts came from other situations. The car insurance was allowed to lapse, which later led to an accident and costly restitution payments. The vehicle purchase was also connected to transportation needs for medical appointments and everyday family life. Those decisions were made by her fiancé, not by her.

There is also a strong emotional side to this situation. She describes years of criticism from his grandparents. Because of that history, the current disagreement feels about more than money. It feels personal. Instead of seeing her new job as a positive step forward, she feels like they are treating her paycheck as a way to recover money they believe they are owed.

Many people also point out that caregiving has real economic value. Raising a child full-time, especially a child with health concerns, requires time, energy, and constant attention. If the family had hired a nanny, caregiver, or childcare professional, the cost could have been significant. Family finance experts often note that stay-at-home parents contribute important value to the household even when they are not bringing home a paycheck.

That is why many readers are concerned about the expectation that she should hand over her entire income. There is a big difference between helping with family finances and giving away every dollar earned. Most couples work together on budgeting, debt repayment, and financial planning. However, financial independence is also important, especially for someone returning to work after years of caregiving responsibilities.

Another important detail is that she is not refusing to contribute financially. She has already said she wants to help with household expenses, family budgeting, and long-term financial goals. What makes her uncomfortable is the expectation that all of her income should go directly toward debts she never personally agreed to take on.

Her age and life situation also matter. She became a parent at a very young age and spent years balancing caregiving responsibilities, medical appointments, and family challenges. That is difficult for anyone. Building financial stability under those circumstances is not easy, and many young families face similar struggles.

Some people have suggested extra jobs or side income opportunities, but not every option is realistic. Caregiving duties, health challenges, transportation needs, and accessibility concerns can all limit earning opportunities. Financial hardship is rarely as simple as “just work more.”

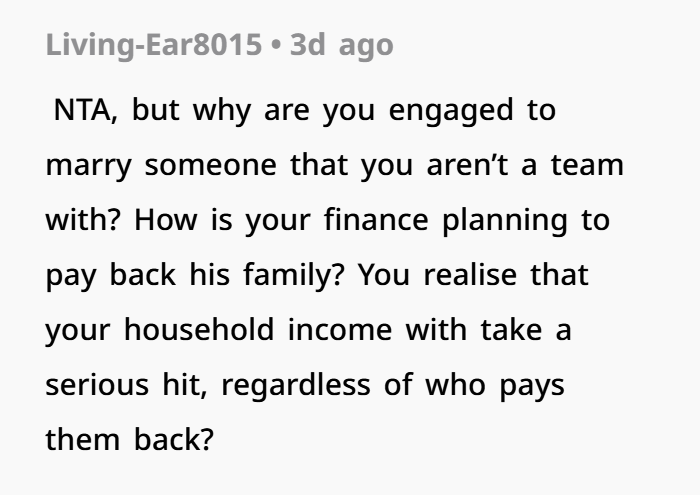

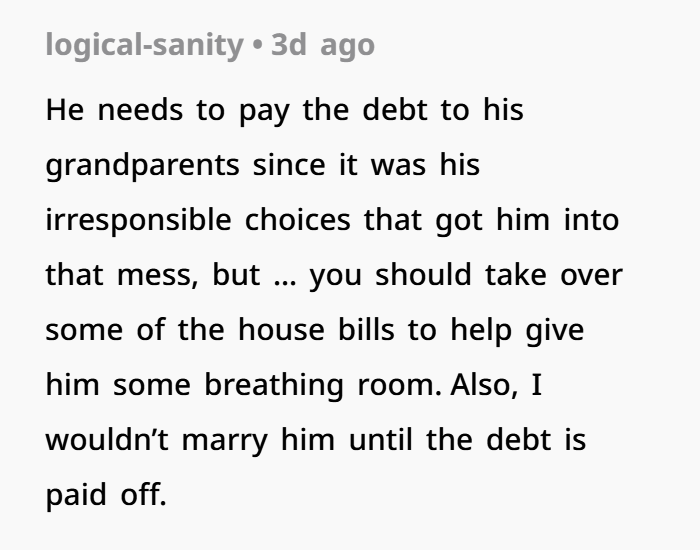

Another question many readers have is about her fiancé’s role in all of this. These debts belong to him, and the financial arrangements were made between him and his grandparents. Because of that, many people believe he should be the one setting expectations and creating healthy boundaries. Strong communication is important in any relationship, especially when family finances are involved.

Money management remains one of the biggest challenges for many couples. Adding pressure from extended family can make those conversations even harder. If one partner feels blamed for decisions that were made together, resentment can grow quickly.

Many people also recognize that financial help from family sometimes comes with expectations attached. The grandparents may feel they stepped in during difficult times and now want repayment. Their feelings are understandable. However, there is still a difference between asking for reasonable help and demanding complete control over someone else’s income.

This is why the story connects with so many readers. It reflects larger conversations about childcare costs, caregiving responsibilities, family budgeting, financial planning, and financial independence. Many stay-at-home parents make sacrifices that help their families survive difficult periods, only to face criticism later for those same sacrifices.

At the end of the day, this does not sound like someone avoiding responsibility. It sounds like a young mother trying to build financial stability, support her family, and protect her future. Most readers can see the difference between being irresponsible and simply trying to create a healthier financial path forward.

See The Comments Below

Most people reading this situation will probably agree that contributing to household finances now that she’s working makes sense. But expecting her entire income to go toward debts she never personally created or agreed to repay crosses a line for many. Especially after years spent raising their child and managing medical needs.

The bigger issue here may not even be the money itself. It’s the resentment, blame, and control attached to it. And unless the couple gets on the same page fast, that tension is only going to grow once the paychecks start coming in.